Cyber threats are no longer a distant risk—they’re an everyday reality for businesses of all sizes.

Hackers target companies with ransomware, phishing scams, and data breaches, often leaving them with massive financial losses and operational disruptions. The worst part? Many businesses assume they’re protected under their cyber insurance policy, only to discover critical gaps when it’s too late.

In 2024, data breaches cost businesses an average of $4.88 million, putting immense financial pressure on companies struggling to recover (IBM Cost of a Data Breach Report 2024). Without the right cyber insurance coverage, your business could face devastating losses with no safety net to fall back on.

| As Shaun Davis, CSO of Netsurit, says, “Cyber insurance is not just a policy—it’s a financial safeguard against evolving threats. Understanding your coverage is the key to real protection.” |

This guide will walk you through why cyber insurance is essential, key policy requirements you should look for, and a cyber insurance coverage checklist to help ensure your business is fully protected.

Why Cyber Insurance is Essential for Your Business

Cybercrime is no longer just a concern for big corporations—small and medium-sized businesses (SMBs) are just as vulnerable if not more. Attackers know that smaller businesses often lack robust cybersecurity defenses, making them easy targets.

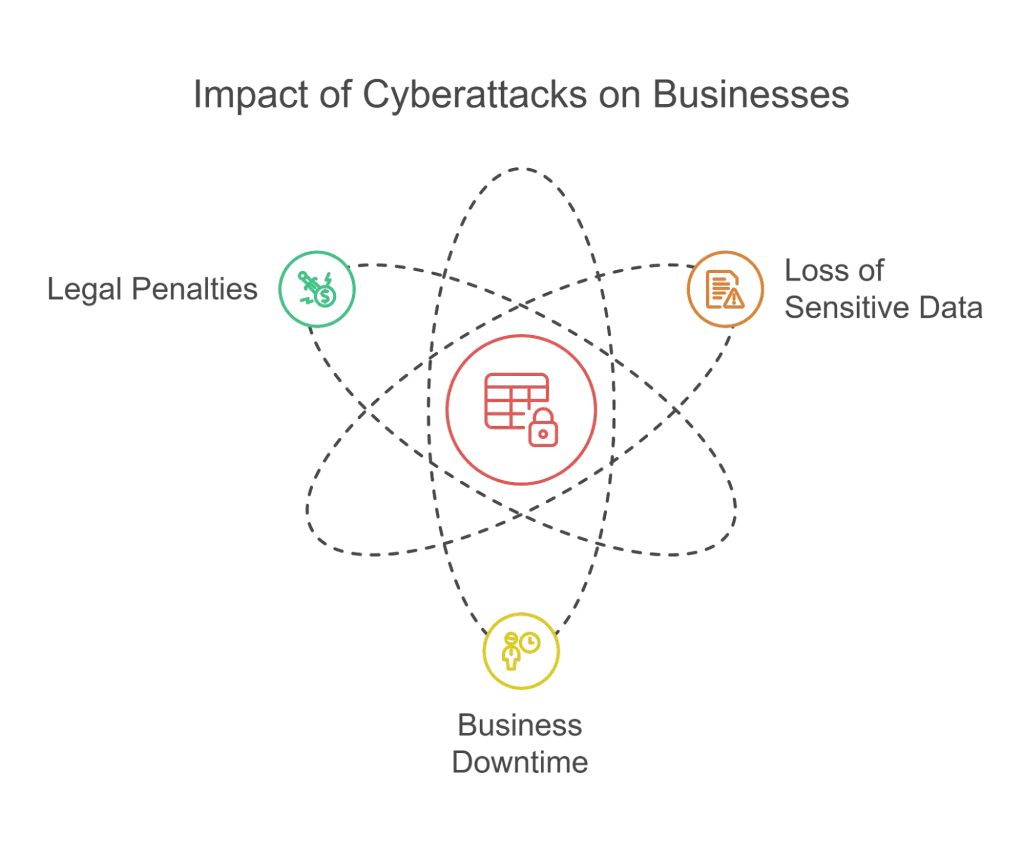

A cyberattack can disrupt your entire operation, leading to:

✔️ Loss of sensitive data – Customer and employee records, financial information, and trade secrets can all be exposed.

✔️ Severe business downtime – If ransomware locks your systems, it could take days or weeks to recover.

✔️ Legal and regulatory penalties – Many industries require businesses to protect sensitive data. A breach can result in hefty fines.

Without cyber insurance, your company is responsible for all recovery costs, including legal fees, forensic investigations, customer notifications, and lost revenue. Many businesses struggle to absorb these costs, leading to long-term financial damage—or even bankruptcy. Yet, only 17% of small businesses currently have cyber insurance, compared to 84% of larger organizations. This gap leaves smaller businesses especially vulnerable, making the right coverage essential.

Cyber insurance provides a financial buffer, helping businesses recover faster by covering expenses related to data breaches, cyberattacks, and business disruptions. But not all policies are created equal. Understanding the specifics of your coverage is crucial to avoiding costly surprises when you need protection the most.

Protect Your Business from Costly Cyber Gaps

Hidden exclusions can put your company at risk—get clarity on your coverage now. Learn More

The Cyber Insurance Coverage Checklist: What You Need to Include

A good cyber insurance policy isn’t just about having coverage—it’s about having the right coverage. Here’s a checklist to help you assess whether your policy is comprehensive:

1. Data Breach & Incident Response Coverage

A cyberattack can expose customer data, trigger legal obligations, and require costly forensic investigations. Your policy should cover:

- Breach response team – Cybersecurity experts who investigate and contain breaches.

- Customer notification services – Required under data protection laws.

- Credit monitoring for affected individuals – Helps prevent identity theft after a breach.

2. Business Interruption & Ransomware Protection

Cyberattacks can halt operations, resulting in revenue loss and hefty ransom demands. Make sure your policy includes:

- Lost income reimbursement – Covers revenue lost due to system downtime.

- Ransomware attack coverage – Pays for ransom demands, if necessary.

- IT restoration expenses – Covers costs to repair or replace compromised systems.

3. Legal & Regulatory Cost Coverage

Lawsuits and fines after a breach can be devastating. Ensure your policy includes:

- Legal defense fees – Covers costs if sued for negligence.

- Regulatory compliance fines – Pays penalties for failing to protect data.

- PR & reputation management – Helps mitigate negative press and restore customer confidence.

4. Cyber Extortion & Fraud Protection

Hackers don’t just steal data—they manipulate businesses into fraudulent transactions. Your policy should protect against:

- Social engineering fraud – Covers losses from email scams and impersonation attacks.

- Wire transfer fraud – Protects against fraudulent fund transfers.

- Extortion demands – Pays for costs associated with cybercriminal threats.

5. Network & System Restoration

Getting back to business after an attack is costly. Your insurance should help cover:

- Hardware & software replacements – If systems are damaged beyond repair.

- Data restoration – Recovering lost or corrupted files.

- Ongoing security improvements – Strengthening defenses to prevent future incidents.

Having these coverages in place ensures that your business is protected from financial ruin if a cyberattack occurs. But even with the best insurance, it’s important to take proactive steps to reduce your risk.

Key Cyber Insurance Coverage Policy Requirements

To ensure you’re fully covered, review your policy for these critical protections:

1. First-Party Coverage: Protecting Your Business Directly

First-party coverage helps your business recover from the direct financial impact of a cyberattack. This includes:

- Incident Response & Forensic Investigation: If your systems are breached, your policy should cover the cost of forensic experts to identify how the attack happened and what data was compromised.

- Business Interruption Coverage: A cyberattack can force your business offline for days or even weeks. This coverage compensates for lost income during that downtime.

- Data Recovery & System Restoration: Repairing or replacing damaged IT infrastructure can be expensive. Your policy should cover these costs to get your operations back on track.

2. Third-Party Coverage: Protecting You from Lawsuits & Claims

A cyberattack doesn’t just impact your business—it can affect your customers, partners, and vendors. Third-party coverage protects you from lawsuits and liability claims that arise from an incident. It typically includes:

- Legal Defense Costs: If customers sue for damages after their data is exposed, your insurance should cover legal expenses.

- Settlements & Regulatory Fines: Some breaches result in fines from regulatory bodies (GDPR, CCPA, HIPAA). Your policy should help cover these penalties.

- Public Relations & Reputation Management: A breach can damage customer trust. Some policies include PR services to help rebuild your reputation.

3. Compliance & Regulatory Coverage: Meeting Legal Requirements

Businesses in industries like healthcare, finance, and retail must comply with strict data protection laws. Your cyber insurance should cover:

- Breach Notification Costs – Many regulations require notifying affected individuals after a breach, which can be expensive.

- Regulatory Investigations & Fines – Covers legal defense and penalties if authorities investigate your compliance practices.

Without these protections, your business could face severe financial and legal consequences after a cyber incident.

Cyber Insurance Coverage vs. No Coverage (Impact of a Cyberattack)

| Scenario | With Cyber Insurance | Without Cyber Insurance |

| Data Breach Response | Covered – forensic investigation & breach response | Out-of-pocket costs for investigation & response |

| Business Downtime | Lost revenue compensated | Revenue loss, no financial support |

| Ransomware Attack | Ransom payment & recovery costs covered | Pay ransom or lose access to critical systems |

| Regulatory Fines & Lawsuits | Legal defense & fines covered | Full liability, expensive legal battles |

| Reputation Management | PR & crisis management included | Negative impact with no support |

| More articles you might like: |

Protect Your Business with the Right Cyber Insurance Coverage

Cyber insurance is more than just a policy—it’s a critical safeguard against the financial and operational fallout of a cyberattack. But too many businesses assume they’re fully covered, only to realize their policy has gaps when it’s too late. Following this cyber insurance coverage checklist ensures you have the right protection in place before a breach happens, not after.

Netsurit helps businesses navigate complex cyber insurance policies, ensuring they meet insurer requirements and strengthen their security defenses. Don’t leave your business exposed. Contact us today to review your cyber insurance strategy and secure complete coverage.

| Discover Trusted Cybersecurity Services Near You | |