Why Technology Is No Longer Optional for Accounting Firms

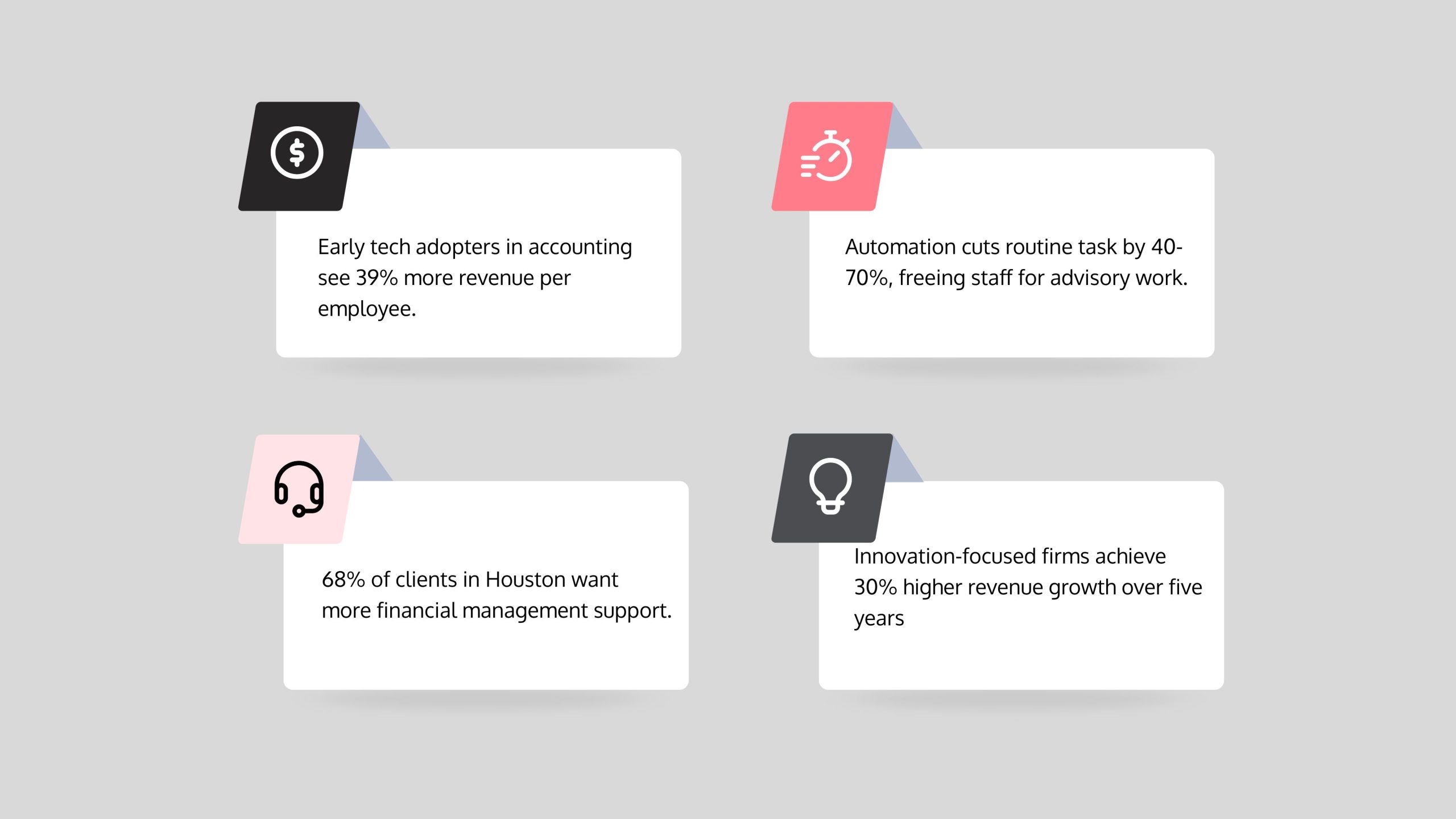

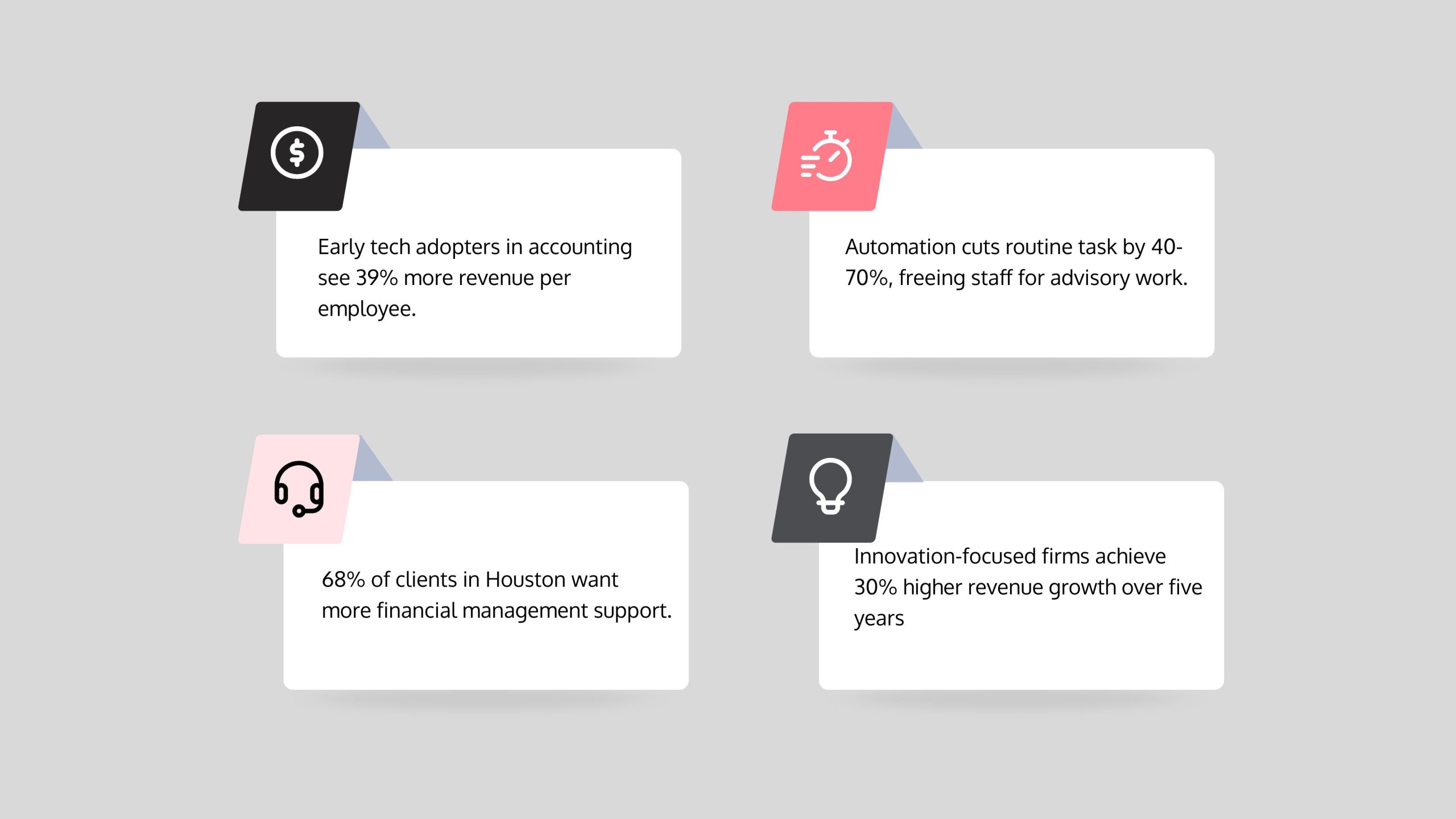

Why is technology a competitive advantage for accounting firms? Because it delivers three measurable benefits: automation frees staff from repetitive work (firms report cutting scheduling time from 1–5 hours to under 1 hour per week after adoption), cloud tools strengthen client relationships (68% of clients now demand more financial management support), and data analytics open up new advisory revenue innovation-focused firms seeing (30% higher revenue growth over five years). Early adopters in the U.S. make 39% more revenue per employee than their peers.

Quick Answer: The Three Tech Advantages

- Automation – Cut time on data entry, reconciliations, and report generation by 40–70%; reallocate staff to advisory work.

- Cloud Collaboration – Serve clients anytime, anywhere with secure portals; reduce status-update calls and improve responsiveness.

- Data Analytics – Move from compliance to strategic advice; spot trends, forecast outcomes, and drive client profitability.

Many accounting firms in the Greater Houston area—from Sugarland to Conroe to Katy—feel overwhelmed by the pace of tech change. The good news? You don’t need to adopt every new tool. The real advantage comes from three focused shifts: automating routine work, improving client collaboration with cloud platforms, and using data to deliver sharper, forward-looking advice. These aren’t just efficiency gains—they’re strategic moves that future-proof your firm and open new revenue streams.

I’m Orrin Klopper, CEO of Netsurit, and over the past 29 years I’ve helped more than 300 organizations—including dozens of accounting firms—modernize their IT to stay competitive and secure. Through that work, I’ve seen why technology is a competitive advantage for accounting firms: it transforms how you serve clients, manage risk, and grow profitably. Let’s walk through the three painless ways you can put that advantage to work.

1. Automate Routine Work to Free Up Staff for Higher-Value Tasks

Most accounting firms know the problem intimately: your best people spend hours on data entry, invoice matching, bank reconciliations, and report generation. These tasks must get done, but they don’t require a CPA’s expertise. That’s why is technology a competitive advantage for accounting firms—automation software, AI, and workflow tools now handle this repetitive work, freeing your team to focus on analysis, strategy, and client relationships.

The numbers tell the story. Before automation, 46% of Houston-area CPAs spent 1–5 hours every week just on scheduling and updating work status. After implementing workflow automation, 34.8% cut that time to under an hour, and another 33.5% spend less than an hour updating work progress. That’s not a minor efficiency gain—it’s 3–4 hours per person, per week, redirected toward activities that actually grow your firm.

A Sugarland firm we worked with saw this firsthand. Their junior accountants were drowning in accounts payable processing for a dozen small-business clients. Manual data entry, three-way matching, approval routing—it consumed 15–20 hours per week across the team. They deployed an intelligent AP automation platform that handled invoice capture, matching, and routing. Processing time dropped 70%. More importantly, one of those junior accountants now spends her time running cash flow analyses for clients, spotting liquidity issues two or three months before they become crises. The firm turned a cost center into an advisory revenue stream, and the accountant is far happier doing work that requires her judgment, not just her typing speed.

How Automation Changes Daily Accounting

Automation doesn’t eliminate work—it eliminates the wrong work. Instead of manually matching receipts or copying numbers between systems, your staff oversees the process, reviews exceptions, and interprets what the data means. That shift reclaims hours for advisory conversations, complex problem-solving, and the kind of proactive service that keeps clients loyal.

Take monthly reporting. Many firms still have someone pull data from the accounting system, modify it in Excel, add commentary, and email it to the same five people every month. Modern tools can automate every step: scheduled extraction, change with Power Query or SQL, and delivery to a secure portal or inbox. Your team reviews the output for accuracy and anomalies, then spends their time explaining what those numbers mean and what the client should do next. That’s the work clients value—and the work that justifies higher fees.

The trade-offs are real, though. Automation works best when your tasks are high-volume, rule-based, and repetitive—reconciliations, standard reports, payroll runs, expense categorization. Avoid it when the work demands nuanced judgment, variable client preferences, or complex human interaction. The risks include automation bias (when teams stop checking outputs and errors compound), data silos from poorly integrated tools, and the upfront cost and learning curve. To mitigate those risks, schedule regular human reviews of automated outputs, choose platforms with strong APIs so your tools talk to each other, and follow a structured Digital Transformation Framework to phase in changes without disrupting client service.

The bottom line: automation isn’t about replacing accountants. It’s about letting accountants be accountants—advisors, strategists, problem-solvers—instead of data clerks. Firms that make that shift see their staff happier, their clients better served, and their revenue per employee climb. That’s a competitive advantage you can measure.

2. Use Cloud Tools to Strengthen Client Relationships

Your clients don’t work nine-to-five anymore, and they don’t want to wait until Monday morning to see their numbers. Cloud platforms, secure portals, and real-time collaboration tools let you meet them where they are—whether that’s a coffee shop in Katy at 6 a.m. or a hotel room in Dallas at 10 p.m. This isn’t about chasing every ping; it’s about building relationships on transparency and accessibility.

The numbers tell the story: 68% of clients in the Houston area want more financial management support, and the best way to deliver that support is through seamless digital communication. When clients can log in, see their documents, check project status, and review dashboards without waiting for a callback, they feel more in control. And when they feel in control, they trust you more. That trust is why technology is a competitive advantage for accounting firms—it transforms the client experience from transactional to strategic.

Consider a CPA firm in The Woodlands serving a mix of real estate investors and small business owners. Before moving to the cloud, their tax season was a storm of phone calls: “Did you get my receipts?” “What’s the status of my return?” “Can you send me last year’s K-1 again?” After implementing a secure client portal and cloud-based accounting software, the firm centralized all document exchange and status updates. Clients could upload receipts, approve documents, and view reports 24/7. The result? A 40% reduction in status-update calls during tax season, freeing staff to focus on complex tax planning instead of playing phone tag. The clients were happier, the staff was less frazzled, and the firm had more capacity for advisory work.

How Cloud Tech Improves Client Service

Cloud technology doesn’t just make your firm more efficient—it makes you look more responsive and proactive. Clients gain on-demand access to their documents, financial dashboards, and real-time updates. No more “I’ll check on that and get back to you.” The information is already there, waiting for them. This immediacy builds trust and signals that you’re a modern, forward-thinking partner.

Beyond portals, cloud-based accounting solutions enable your team to collaborate seamlessly, regardless of location. Your senior accountant in Sugarland can review a file while your manager works on it from Conroe, and your client can approve changes from their phone. This flexibility isn’t just convenient—it’s essential for attracting top talent who value remote work options and for maintaining continuity during disruptions (weather, illness, or the next unexpected event).

Cloud platforms also integrate with other financial systems, giving you a holistic view of a client’s financial health. Instead of toggling between three different software packages, you can pull data from their bank, payroll, and invoicing systems into one dashboard. This streamlined approach means less friction for clients and more time for you to deliver meaningful insights. When you can spot a cash flow issue before the client even asks, you’ve moved from compliance to true advisory—and that’s where the new revenue lives.

Trade-offs Box:

- Works best when: Clients are remote, need frequent data sharing, or want proactive advisory services. Also ideal for firms with distributed teams or seasonal workload spikes.

- Avoid when: All clients insist on paper-based processes (though this is increasingly rare in a tech-savvy market like Houston).

- Risks: Poorly designed portals frustrate users and reduce adoption; data breaches or security vulnerabilities threaten client trust and your firm’s reputation; over-reliance on cloud providers without backup plans.

- Mitigations: Choose user-friendly, secure platforms with strong encryption and multi-factor authentication; provide clear client onboarding and training (a 15-minute walkthrough pays dividends); invest in regular Cyber Security Consulting and IT audits to ensure continuous protection; maintain offline backups of critical data.

3. Turn Data into Strategic Advice for Clients

The accounting profession is shedding its old skin. For decades, we focused on historical record-keeping and compliance—essential work, but backward-looking. Today, the real value for clients lies in changing raw financial data into actionable, strategic advice that shapes their future. Data analytics and AI-powered insights are the engines driving this shift, and they represent one of the clearest answers to why is technology a competitive advantage for accounting firms.

Firms that accept this data-driven approach see tangible results. McKinsey reports that companies prioritizing innovation outperform their peers by 30% in revenue growth over a five-year period (US, 2023–2028). This substantial growth stems largely from offering sophisticated, data-driven advisory services that go beyond basic accounting. These firms interpret numbers to identify trends, forecast outcomes, and uncover opportunities that directly impact client profitability. They’re not just processing transactions; they’re guiding business strategy.

Consider a Katy-based accounting firm working with a retail client. Traditionally, they might have reviewed quarterly financial statements and noted declining profit margins—then filed the report. With advanced data analytics tools, they went deeper. They analyzed sales data by product line, correlated it with marketing spend, and compared performance against local market trends. The result? They spotted that a specific product category was underperforming due to outdated inventory and inefficient pricing. Instead of just reporting the problem, they presented a strategic plan to optimize pricing, refresh inventory, and restructure marketing efforts. This led to a new engagement focused on ongoing business optimization, significantly boosting the client’s profitability and solidifying the firm’s role as a trusted strategic advisor—not just a compliance provider.

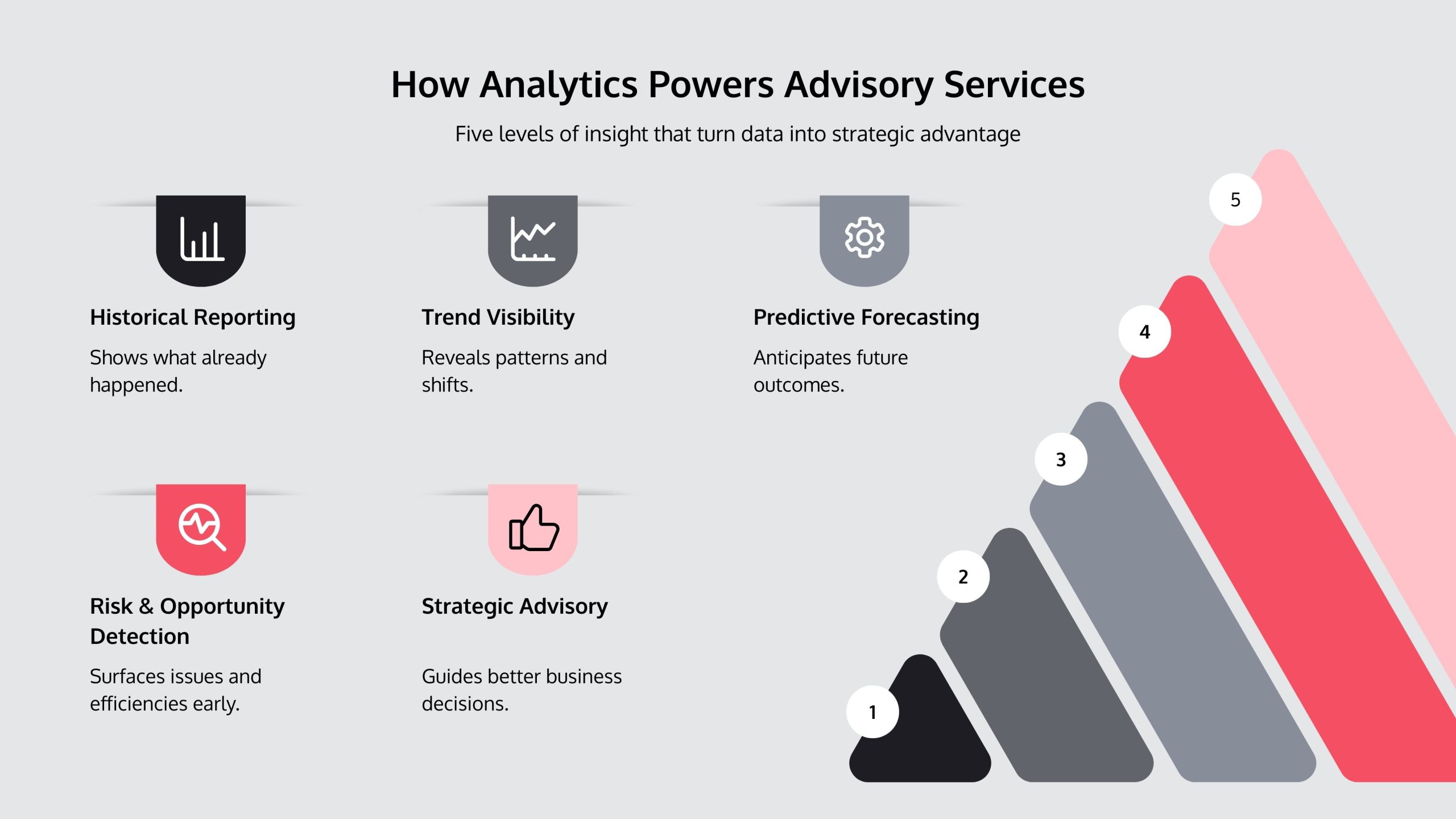

How Analytics Powers Advisory Services

AI and data analytics enable accountants to deliver forward-looking advice, rather than just historical reports. We can now use predictive modeling to anticipate cash flow shortages, identify potential tax liabilities before they arise, and forecast the impact of different business decisions. This proactive approach helps clients make informed choices, mitigate risks, and seize opportunities they might otherwise miss.

AI tools can rapidly process vast amounts of financial data, identifying patterns and anomalies that human eyes might overlook. This capability proves invaluable for fraud detection, compliance monitoring, and uncovering hidden efficiencies. For a Conroe firm serving manufacturing clients, analytics revealed that invoice payment delays were costing clients thousands in missed early-payment discounts. The firm built a dashboard to track and optimize payment timing, turning a compliance task into a profitability driver.

By leveraging these insights, we provide customized advice based on deep data analysis—ranked as a top competitive advantage by accountants in recent surveys. This level of insight lifts our role from financial scorekeepers to indispensable strategic partners. Clients don’t just want to know what happened last quarter; they want to know what’s coming and how to prepare. That’s the advisory edge that data delivers.

Trade-offs Box:

- Works best when: The firm wants to offer strategic advisory services, has access to clean and reliable client data, and is committed to continuous learning and staff development.

- Avoid when: Staff lack fundamental data literacy and analytics skills, or client data is consistently messy, incomplete, or siloed across disparate systems that don’t communicate.

- Risks: Bad data leads to bad advice (garbage in, garbage out); overfitting trends can result in inaccurate predictions; privacy concerns if data handling protocols are not robust.

- Mitigations: Invest in training staff in data literacy and analytics tools; start with a Productivity Assessment to clean up and standardize data sources; implement strong data governance and anonymization practices where appropriate.

Why Tech Is a Strategic Advantage for Houston Accounting Firms

Technology adoption isn’t just about buying new software or subscribing to the latest cloud service. It’s a strategic decision that determines whether your firm will thrive five years from now or struggle to keep up. For accounting firms across the Houston metro area—from downtown offices to practices in Sugarland, Conroe, and Katy—why is technology a competitive advantage for accounting firms boils down to three realities: it future-proofs your business model, helps you compete for scarce talent, and protects you against mounting digital risks. Firms that accept technology thoughtfully are building resilience against economic uncertainty, talent shortages, and evolving client expectations.

Overcoming Adoption Barriers: A Houston Firm’s Plan

We understand the hesitation. Budget constraints are real, especially for smaller and mid-sized firms. The perceived lack of in-house IT expertise can feel like a roadblock. And the sheer pace of technological change—new tools, new regulations, new threats—can be overwhelming. Thomson Reuters data confirms that keeping up with the latest developments and ensuring compliance with evolving regulatory standards requires continuous learning and rapid adaptation. These aren’t small challenges.

But they’re not impossible, either. The firms we’ve worked with that succeed take a phased approach. Instead of attempting a complete technology overhaul overnight, they implement changes incrementally. Maybe they start with automating invoice processing, then add a client portal, then layer in analytics tools six months later. This gives staff time to adapt, builds confidence, and delivers measurable wins that justify the next investment.

Targeted training makes a huge difference. Your team needs both technical skills—how to use the new software—and softer capabilities like prompt engineering for AI tools or interpreting data visualizations. And here’s the reality: you don’t need to build this expertise entirely in-house. Partnering with experienced IT professionals can bridge the gap. Our IT Strategy Services help Houston-area firms develop a clear, realistic roadmap for technology adoption. We align investments with your business goals and client needs, so you’re not overwhelmed and your internal team can stay focused on serving clients. This external partnership lets you benefit from cutting-edge technology without hiring a full IT department.

Security and Compliance: Non-Negotiable for Digital Firms

As your firm moves more operations online and handles increasing volumes of sensitive financial data, security and compliance shift from background concerns to front-and-center priorities. According to Statista, the financial industry is the second-most targeted sector for cybercrime. For accounting firms, that’s not an abstract statistic—it’s a daily threat. A single data breach can destroy a firm’s reputation, trigger regulatory penalties, and shatter the trust clients have built with you over years. This is a critical reason why is technology a competitive advantage for accounting firms: robust security protects your most valuable assets—your data and your reputation.

Technology itself is both the risk and the solution. Secure file-sharing platforms with end-to-end encryption, multi-factor authentication (MFA), automated backup systems, and regular security audits are no longer optional. They’re table stakes. But tools alone aren’t enough. You also need a comprehensive cybersecurity risk management framework. The AICPA’s System and Organization Controls (SOC) for cybersecurity provides a proven blueprint for managing and reporting on cybersecurity risks. It helps firms demonstrate to clients and regulators that they’re serious about protection.

Investing in Cyber Security Consulting and regular audits isn’t just about avoiding disasters. It’s about building a competitive advantage. Clients increasingly ask about your security practices before they sign. Being able to show a robust, audited framework gives them confidence and sets you apart from firms that treat security as an afterthought. In a market as competitive as Houston, that peace of mind can be the deciding factor for a new client.

The Future-Proof Accountant: Skills and Strategy

The role of the accountant is changing rapidly, and the skills that made someone successful a decade ago won’t be enough going forward. Manual data entry and historical reporting are being automated. The future-proof accountant needs a broader, more strategic skill set: data analysis, fluency with cloud-based systems, and even emerging capabilities like prompt engineering—the art of asking AI tools the right questions to get useful answers.

The World Economic Forum’s 2023 Future of Jobs Report makes this clear. Jobs that rely on “human skills such as judgment, creativity… and emotional intelligence” are far less likely to be automated. Technology doesn’t replace accountants; it amplifies what makes them valuable. By automating routine tasks, technology frees accountants to spend more time on strategic advisory services—an average of 47% of their time, according to recent surveys. That’s where the real value lies, both for clients and for your firm’s revenue.

This shift requires intentional investment in training and culture. Your team needs to develop critical thinking, problem-solving, and communication skills alongside their technical accounting expertise. Encourage curiosity about data. Create space for staff to experiment with new tools. And recognize that continuous learning is now part of the job description, not an occasional perk. Firms that build this culture will attract and retain the best talent, because top accountants want to work where they can grow, not where they’ll spend their days fighting with spreadsheets.

Houston’s accounting market is competitive and fast-moving. The firms that will lead in 2026 and beyond are the ones investing now in the right technology, the right security, and the right skills. That investment doesn’t have to be overwhelming—but it does have to be strategic and sustained.

Conclusion

Why is technology a competitive advantage for accounting firms? Because it fundamentally reshapes how you operate, serve clients, and grow. For accounting firms across Houston—whether you’re downtown, in Katy, Sugarland, or Conroe—the evidence is clear: technology delivers efficiency through automation, builds stronger client relationships via cloud collaboration, and opens new advisory revenue streams through data analytics. These aren’t minor tweaks to your workflow. They’re strategic shifts that determine whether your firm thrives or struggles over the next five years.

The firms we work with that accept technology strategically don’t just save time. Firms transform their service model, moving from reactive compliance work to proactive advisory that genuinely impacts their clients’ bottom lines. They attract better talent because they offer modern tools and flexible work arrangements. They protect client data with robust security frameworks. And they position themselves to adapt quickly as client expectations and regulatory requirements continue to evolve.

Here’s what matters most: you don’t need to overhaul everything at once. Start where you’ll see the fastest return—maybe that’s automating your accounts payable workflow, implementing a secure client portal, or cleaning up your data so you can offer meaningful analytics. The key is to start with a clear plan.

Ready to map your firm’s technology roadmap? Book a professional IT Audit and Assessment to identify your highest-impact opportunities. Then see how Netsurit’s Accounting Firm IT Services can help you implement those changes smoothly, securely, and without disrupting your daily operations. Your competitive edge is waiting.